PROJECTS

BITCOIN WALK FORWARD ANALYSIS - Random forest model

PROJECT SUMMARY

This is my first project using machine learning models. I will use the Random forest model on past Bitcoin price data to try to predict if the price of Bitcoin will go up tomorrow by 2%.

I collected the neccessary data from yahoo finance and ran add_all_ta_features on the dataframe to get the the indicators i will need. After that I added custom features reccomended by ChatGPT, set the target, prepared the data for the model and split the target column from the features.

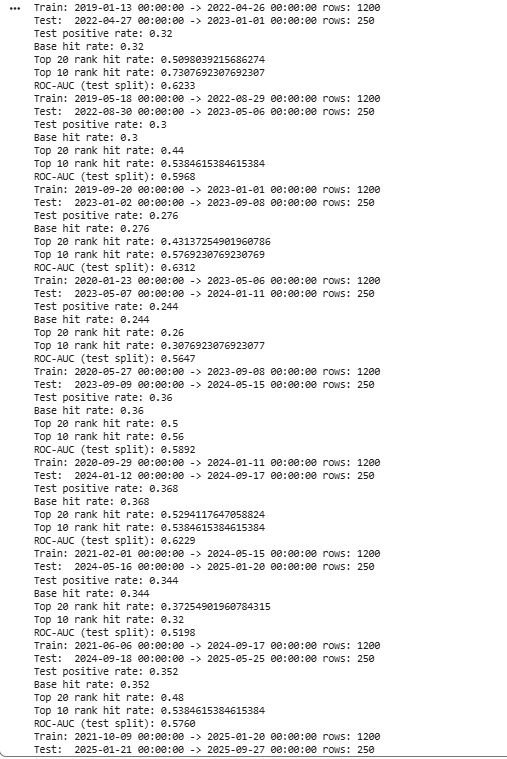

I then created a walk forward analysis using a while loop where I ran the model and collected important data like ROC_AUC score and top 10% hit average.

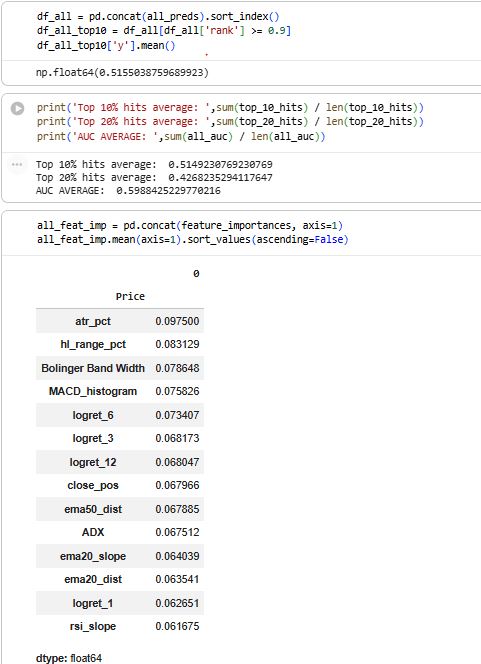

In out-of-sample testing, the model’s highest-confidence 10% of signals achieved a 51.5% hit rate for reaching a +2% move, significantly outperforming the baseline probability.

Github link – https://github.com/Cadez123/BTC_random_forrest_walk_forward_analysis.git

DETAILED DESCRIPTION

1) Import libraries

Loads Python packages for:

data handling (pandas, numpy)

market data download (yfinance)

technical indicators (ta)

ML + evaluation (scikit-learn)

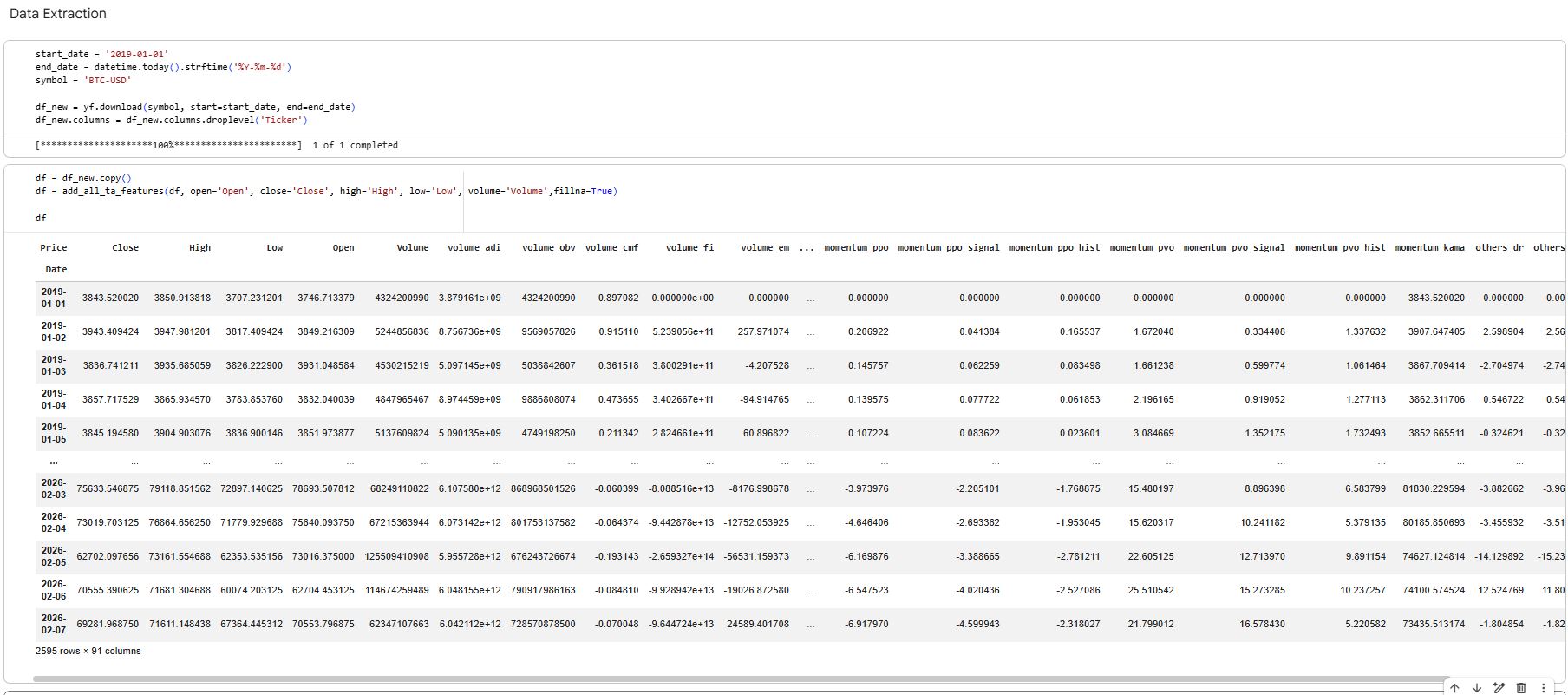

2) Download daily OHLCV data

Pulls BTC-USD daily candles from Yahoo Finance for a chosen date range.

Creates a clean price DataFrame with Open, High, Low, Close, Volume indexed by date.

3) Generate technical indicator features

Uses

ta.add_all_ta_features(...)to calculate a large indicator set (trend, momentum, volatility, volume-based indicators).Adds extra custom features on top:

log returns over multiple horizons

EMA distance, EMA slope

RSI slope

MACD histogram

ATR %

Bollinger Band width

ADX

candle structure features like high-low range and close position in candle

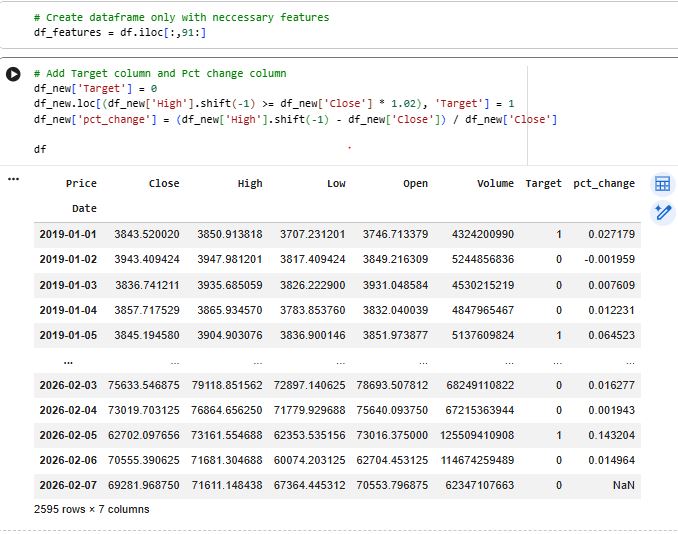

4) Select the feature set

Slices out the final feature block (

df_features = df.iloc[:, 91:]) to keep only the engineered features used for modeling.

5) Create the prediction target

Defines the classification label:

Target = 1 if next day HIGH ≥ today CLOSE × 1.02

else Target = 0

Also computes a helper column (

pct_change) to inspect the size of next-day moves.6) Build the modeling dataset

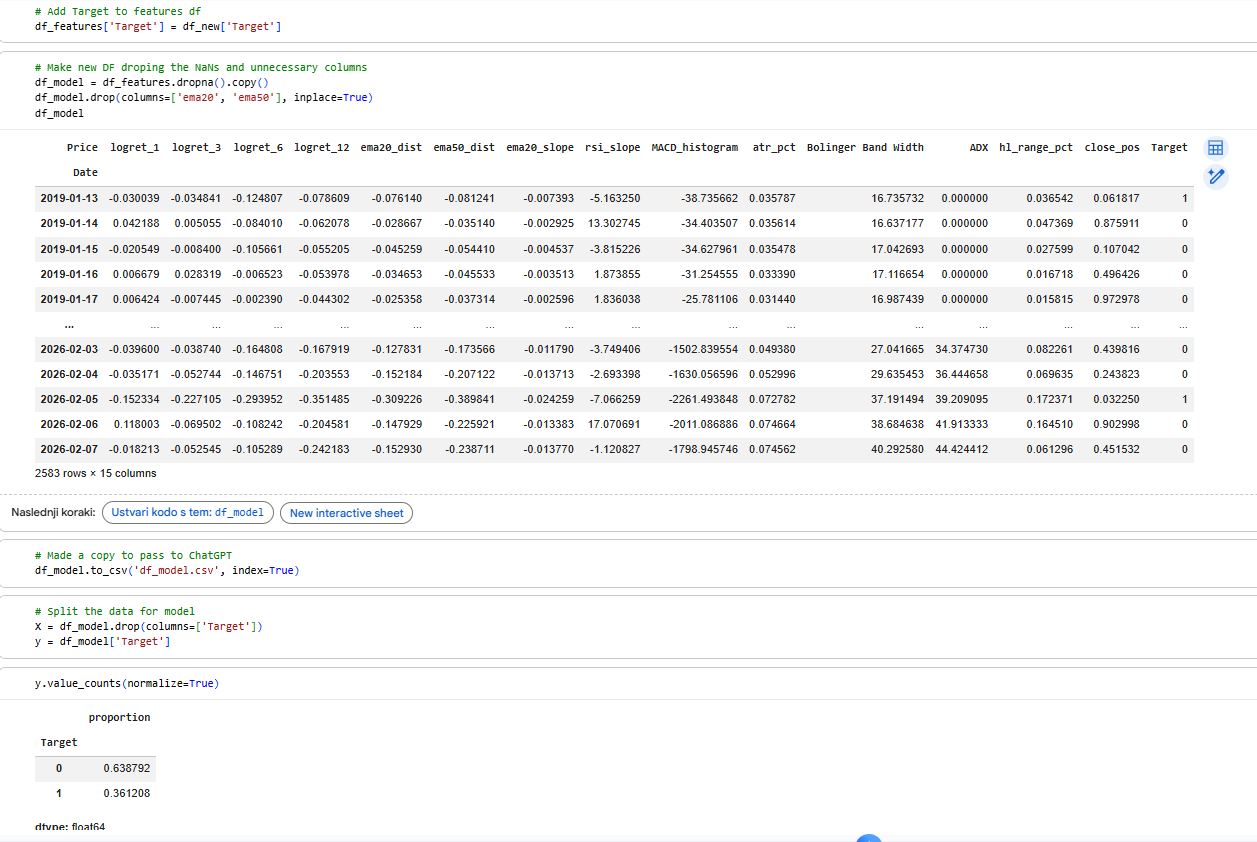

Attaches

Targetto the feature table.Drops NaNs caused by indicator warm-up periods and shifting.

Drops a couple of unused columns (like

ema20,ema50) for the final model table.Exports the final dataset to CSV (

df_model.csv) for reuse/sharing.

7) Split inputs and outputs

Separates:

X= all feature columnsy= the Target column

Runs sanity checks:

same length, aligned index, time-ordered, no missing values

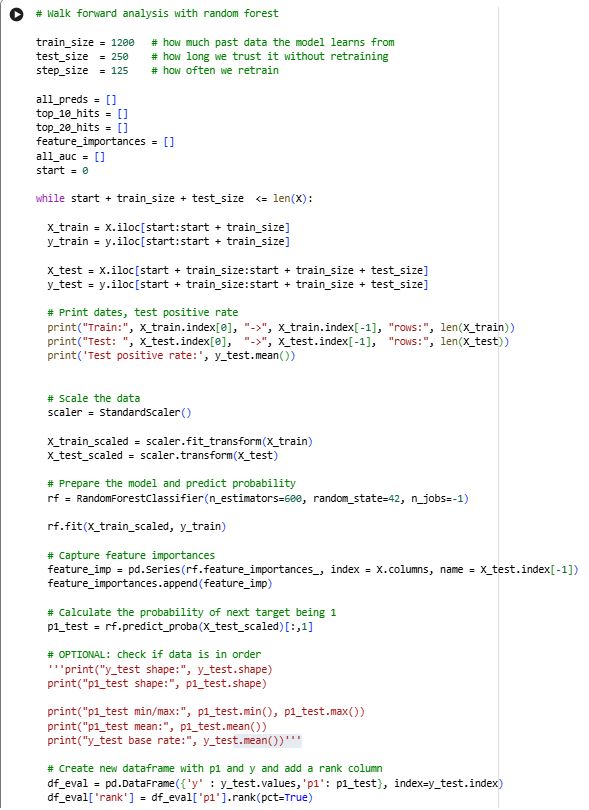

8) Walk-forward training (time-series backtest)

Implements a realistic “train on past → test on future” loop:

Uses rolling windows:

train_size = 1200test_size = 250step_size = 125

For each window:

Split train/test strictly by time (no shuffling)

Fit

StandardScaleronly on training data (prevents leakage)Train a RandomForestClassifier

Predict probabilities (

predict_proba) for the test windowStore results and metrics

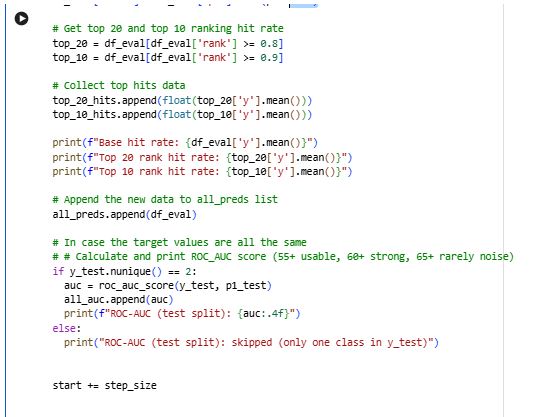

9) Ranking-based evaluation (not fixed thresholds)

For each test window:

Builds

df_evalwith:true label

ypredicted probability

p1

Converts

p1into a percentile rank within that window.Measures how well the model concentrates “wins” in the highest-confidence predictions:

Top 20% hit rate (rank ≥ 0.8)

Top 10% hit rate (rank ≥ 0.9)

10) AUC evaluation per window

Calculates ROC-AUC for each test window (skips windows that contain only one class).

Stores AUCs to later compute the average performance across time.

11) Combine all out-of-sample predictions

Concatenates all window test predictions into

df_all(still out-of-sample only).Computes overall Top-10 performance from

df_all.

12) Feature importance stability across time

Saves

rf.feature_importances_each window.Combines them into a matrix (features × windows).

Computes average importance per feature to see which features stay consistently useful over time.